Using Vertical Integration in Agriculture to Counter Supply Chain Consolidation

Learn how producers can hedge risk in an increasingly consolidated supply chain with vertical integration.

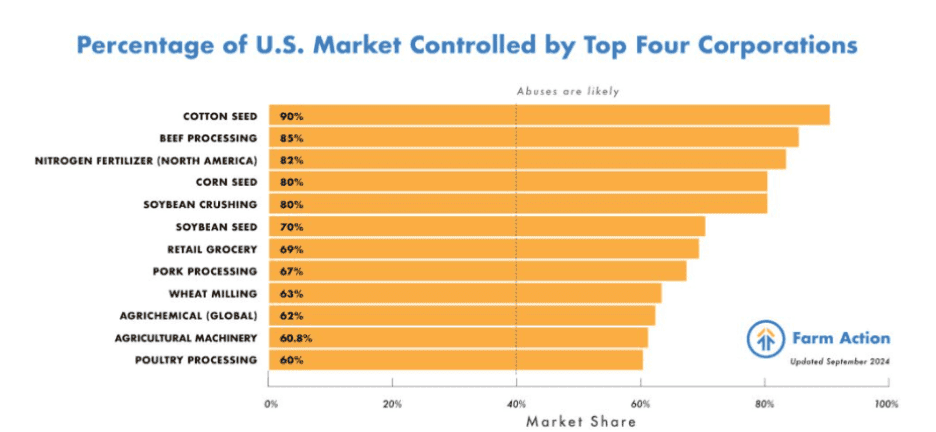

Over the past several decades, consolidation has reshaped nearly every segment of the agricultural supply chain. From seed suppliers and fertilizer manufacturers to meatpackers and food retailers, fewer companies now control larger shares of the market. For producers, that shift often translates into tighter margins and less negotiating power.

Upstream, consolidation among seed, fertilizer, and chemical companies has significantly concentrated input markets. Mergers among major agribusiness firms have reduced the number of major global seed and crop protection providers to just a handful of companies.

Meanwhile, downstream consolidation continues across processing and retail markets. In industries such as meatpacking, for example, a small number of firms control the majority of U.S. processing capacity, leaving producers with limited options in many regions.

This dynamic leaves many farmers and ranchers squeezed between two concentrated segments of the supply chain—the companies that sell inputs and the companies that purchase agricultural commodities.

The Economics Driving Vertical Integration in Agriculture

The economics of the U.S. food system reflect that imbalance. Most recent data indicates that, on average, farmers and ranchers received approximately 11.8 cents of every dollar spent on domestically produced food. The remaining share goes toward marketing, processing, transportation, packaging, and retail services.

On the input side, seed, fertilizer, and chemical markets have experienced major consolidation over the past three decades. Many farmers believe this consolidation has contributed to higher input prices and reduced competition.

“They went from roughly 20 companies 30 years ago down to four. Every time there was a merger, they said they’d pass the savings down to the customer. That hasn’t happened.”

– Mark Mueller, Iowa Farmer

Fewer suppliers mean reduced negotiating power for farmers, but also greater vulnerability to global disruptions—such as geopolitical conflicts affecting fertilizer supply—that trigger rapid price spikes.

But consolidation trends don’t stop there. Concentration is also evident further down the supply chain. Meatpacking, grain processing, and food retail sectors are also dominated by a shrinking number of companies. The American farmer is being squeezed from both ends.

“For 40 years we’ve been ignoring antitrust laws in this country, and it’s led to major consolidation. We don’t have the competition, especially in the fertilizer market, that we used to and that drives up prices. It gives manufacturers market power.”

– Lance Lillibridge, Iowa Farmer

In response, more producers are exploring vertical integration in agriculture to protect margins, gain leverage, manage risk, and improve market access.

What Is Vertical Integration in Agriculture?

In simple terms, vertical integration in agriculture is a business strategy in which a farm operation manages multiple stages of the agricultural supply chain to reduce reliance on external suppliers, processors, or distributors. It allows farmers to control more stages of production, processing, and distribution, thereby improving margins and lowering market risk.

Rather than simply producing a commodity and selling it into the marketplace, vertically integrated farms may handle additional steps such as input sourcing, storage, processing, or direct marketing.

Here are some of the most common forms of vertical integration in agriculture.

1. Upstream Integration (Inputs)

Some producers move upstream by controlling a greater share of their input supply.

Examples include:

- On-farm seed production

- Custom fertilizer blending

- Livestock breeding programs

- Feed production

These strategies can help reduce dependence on external suppliers and provide more control over input quality and availability.

2. Midstream Integration (Processing and Storage)

Other operations integrate processing or storage capabilities.

Examples include:

- On-farm grain storage

- Custom milling

- Livestock finishing operations

- Meat processing facilities

- Commodity cleaning or packaging

Midstream integration can give producers greater flexibility over when and how they sell their products.

3. Downstream Integration (Marketing and Distribution)

Some farms integrate further down the value chain by marketing directly to consumers or retailers.

Examples include:

- Direct-to-consumer sales

- Farm-branded food products

- Cooperative marketing programs

- Contract processing

- Regional distribution partnerships

The common objective across these strategies is simple—capture more value from the agricultural supply chain and reduce dependence on external intermediaries.

Agricultural Financing That Supports Vertical Integration Success

Successful vertical integration is rarely a one-season decision. It often requires a thoughtful plan and significant capital investment.

Access to flexible financing is one piece of the puzzle. It provides the capital needed to fund vertical integration initiatives such as processing facilities, grain storage expansions, and more.

But there’s one more piece—the strategic long-term financial plan that can turn your vertical integration goals into success.

These strategies include:

- Phased expansion timelines

- Risk management considerations

- Succession and growth-minded structures

Strategic capital planning allows producers to pursue expansion opportunities without overextending their operations. Working with a financial partner who understands the risk, demand, and importance that comes with building a vertically integrated operation can help.

AgAmerica is a nationwide land lender that specializes in agribusiness finance. We’ve helped operations build processing facilities, secure flexible working capital, and improve loan terms as operational needs evolved.

Ready to take the next step towards financial resilience? Contact us today to get started.