Understanding Ag Land Loan Requirements

Applying for an ag land loan can be intimidating at first, but we’re here to make it as seamless as possible.

It’s important to find a farmland lender that will provide the support you need to understand your options. As one of the leading lenders in the agricultural space, AgAmerica hears many overlapping questions from those seeking a loan to buy agricultural land including:

- What’s the difference between an agricultural land loan and other farm loans?

- What are the requirements for an ag land loan?

- How can I set myself up for success?

- What is the best type of land loan for my needs?

We work hard to educate farmers on their options and what loans for agricultural land they may qualify for. To help get you started, we’ve collected the answers to the most common farm land loan requirement questions we see in the agriculture sector.

Ag Land Loan vs. Farm Operating Loan

Ag land loans and farm operating loans serve different financial needs within the agricultural sector. An agricultural land loan is primarily used to purchase, refinance, or improve farmland and farm-related buildings. The property typically secures this type of loan for agricultural land and offers longer terms, which can help with managing significant capital investments and securing lower interest rates.

The key benefit of an ag land loan is its ability to provide farmers with the financial stability needed to make long-term investments in their land and infrastructure, supporting sustainable growth and operational expansion.

In contrast, a farm operating loan is designed to cover the day-to-day expenses associated with running a farm, such as purchasing seeds, fertilizers, feed, and other essential supplies. These farm operating loans are usually short-term, often revolving, and help manage the cash flow fluctuations that are common in farming due to seasonal income variations.

While both types of loans are beneficial, ag land loans are more resilient to market fluctuations, ensuring that you have the resources needed to expand and improve your operations over time.

Eligibility Requirements for an Ag Land Loan

Most farmland lenders have similar land loan application requirements. You can find general requirements for ag land loans on the AgAmerica website, but exceptions may apply on a case-by-case basis. Typically, if you meet the requirements listed below, you would most likely be eligible to apply for an ag land loan.

- Who Can Apply? – Farmers, ranchers, rural landowners, farm real estate investors, and recreation and timber landowners seeking a loan to buy farmland.

- Land Ownership – To qualify for an ag land loan with AgAmerica, you must own or plan to buy 25 acres or more.

- Minimum Loan Value – AgAmerica land loans start at $50,000.

- Property Value – AgAmerica land loans cannot exceed 75 percent of the land’s value.

- Citizenship – AgAmerica loan recipients must be American citizens or U.S. resident aliens.

Once you’ve established you’re eligible, the next step is to understand what documents will be needed when applying for an ag land loan.

Documentation Requirements for an Ag Land Loan

Not every farmer has a perfectly crafted business plan ready to go or an updated debt schedule laid out. With singular expertise in the ag finance space, we can help you gather the necessary documents to put your best foot forward. The following information is what most agricultural lenders require to approve a farmland loan.

Farm Business Plan

A farm business plan is a detailed document that outlines the goals, objectives, strategies, and financial projections for a business. For farmers, a business plan is a crucial component of the land loan application process because it helps demonstrate the intended use of the loan proceeds and the ability to repay the loan.

A strong farm business plan should include a description of the farming operation, including the type of crops or livestock, the size of the farm, and the markets served. It should also provide an overview of the farmer’s experience and skills, as well as any partnerships or collaborations with other farmers or businesses.

In addition, your farm business plan should outline the intended use of the loan proceeds. This could include purchasing new equipment or land, making improvements to existing facilities, or consolidating debt.

Farm Balance Sheet

An agricultural balance sheet is a financial statement that provides a snapshot of the financial condition of a farm or ranch at a specific point in time. It lists all the assets, liabilities, and equity of the agricultural operation.

A balance sheet can include a detailed debt schedule. A debt schedule lays out all the debt your farm has with related terms such as interest rate, payment amount and frequency, and maturity dates. Usually, lenders ask for this schedule to construct a cash flow analysis.

Some operators update their balance sheet annually, but most farm loan lenders look for a balance sheet that has been updated within the last three months.

Income Statement

Your income statement can be any document that proves your income. Farm loan lenders may ask to see your tax return, a profit and loss statement (P&L), or audited financials.

Verification Statement

A verification statement is usually a bank statement for asset accounts or debt statements. Farm loan lenders will typically ask for these in order to verify your balance sheet accounts.

Financial Projection

Financial projections are a detailed analysis of the farm’s revenue, expenses, and cash flow. It should demonstrate the ability to generate sufficient income to repay the loan, including principal and interest, over the term of the loan.

Ag Land Loan Approval Process

Once eligibility is established and documents are collected, the agriculture loan approval process begins. Every lender has different underwriting processes, and no two organizations are exactly the same. However, these are the factors that most underwriters consider when making a decision on a loan to buy agricultural land.

Debt Service Coverage Ratio (DSCR)

Your DSCR is calculated by dividing your net operating income by your debt obligations. It is used to measure your farm’s ability to produce operational cash flow to support debt obligations.

In general, a DSCR above 1.25 is considered strong. Anything below 1.00 could indicate a farm facing financial troubles.

Debt to Asset Ratio

Your debt to asset ratio measures equity on the balance sheet and is calculated by dividing your total liabilities by your total amount of assets.

This calculation helps land loan lenders understand how highly the operation is leveraged overall.

In general, lenders look for a ratio below 50 percent.

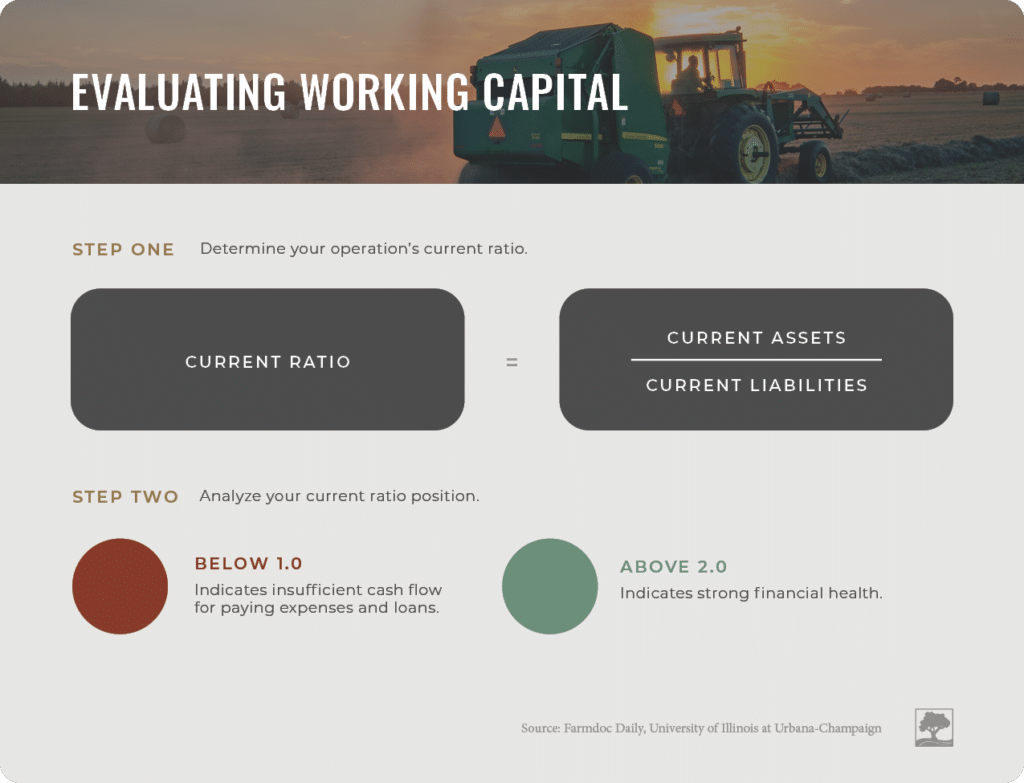

Current Ratio

Your current ratio is what lenders look at to measure your ability to pay short-term debt obligations (usually within the next year).

Your current ratio is calculated by dividing your current assets by your current liabilities.

A low current ratio indicates a weaker working capital position that could pose challenges in paying operating expenses or short-term obligations.

Loan-to-Value (LTV) Ratio

When you’re seeking a loan, it’s important to understand the value of the collateral and how it compares to the loan amount. Most lenders max out at an LTV ratio of 75 percent. This means If your land appraises for $100,000, most lenders are able to give you a loan as high as $75,000.

Credit Score

We understand that farmers and ranchers go through a variety of different circumstances, which can lead to a range of credit scores. When obtaining an agriculture mortgage loan at AgAmerica, we understand that there are a variety of factors that can impact your credit score. As experienced farm loan lenders, we’re more interested in getting the entire picture of your business than relying on just one number. A credit score does impact your loan to buy agricultural land, but it’s still possible to qualify for a loan with a poor credit score.

Custom Agricultural Land Loans to Support Your Farm’s Future

If you’re thinking about applying for a land loan or you just need some answers, don’t hesitate to contact us. At AgAmerica, we prioritize relationships over transactions and are dedicated to keeping agricultural land in the hands of American farm families. To find out if you qualify for one of our customizable farmland loan programs, try our fast track pre-approval farm loan application.