2020 Financial Planning: Alternative Lending as a Financing Source for Your Farm Operation

Alternative Options to Traditional Agricultural Loans.

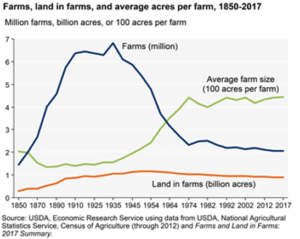

According to the U.S. Department of Agriculture (USDA), farm debt will hit a record high of $416 billion by the end of 2019. Farmers are leaning on lenders now more than ever, not just during the hard times, but to finance new opportunities like farm expansions, equipment updates, and more. So why are farmers choosing alternative lending companies to help open these doors?

Because traditional lenders and banks are tightening their credit qualifications—leaving farmers holding rejected applications instead of much-needed operating capital.

As the national farm debt grows, big bank lenders are making it increasingly difficult for agriculture producers to be approved for traditional loans. In many instances, big bank lenders fall short when it comes to informing their borrowers of alternative funding options. For instance, farm debt consolidation can help make payments more manageable over an extended period of time by refinancing single or multiple loans into a single-term loan. Though this option can require some flexibility in the loan structure, in the end it provides the financial stability that the agriculture producer is seeking. Unfortunately, the industry continues to witness big banks move forward with more foreclosure and bankruptcy each year.

What is Alternative Lending?

If you google “alternative lending” today, you’ll find a lot of mixed reviews. Often, words such as bridge loans and hard money lending pop up, and with it their own set of stigmas.

Some link alternative loan services with incorrigibly high-interest rates. Unfortunately, these types of lending companies do exist and rarely turn anyone away. A substantial portion of these loans go into default because of their lack of financial planning. True alternative lending companies actively fight to destigmatize nonconventional loans in agriculture by repeatedly helping multi-generational farms across the country grow and evolve in today’s industry.

Fighting this stigma is perhaps one of the greatest challenges agricultural lenders face. The limits in regulation that allow for flexible financing, open the floor to several types of alternative lenders, not all of equal value or merit.

As a borrower, it’s important to understand:

1. What alternative lending companies are (and what they aren’t);

2. How alternative lending companies are helping family farms survive; and

3. Why we all should care about the future of these American farms.

Alternative lending is…

Flexible

Lack of regulation allows alternative lending companies more room to create payment plans that work best for the client. For example, debt consolidation with interest-only payments for a certain amount of time can help a financially distressed farmer in ways a traditional loan can’t. These high-yield loans are more collateral-focused and give the borrower a wider capacity to pay loans back.

Customizable

Alternative lending companies understand that every farmer, rancher, producer, and operator is different. Each with their own set of strengths and weaknesses. Once these are established along with company goals, an alternative loan package can be created to suit their specific needs in a way that traditional banks don’t have the freedom to offer.

Personal

Finding an alternative lending company that puts people before profits will make all the difference when an operator is looking for financing options. They take the time to conduct on-site visits of the operation, and consistently check in on clients. Their dedication to helping American farmers is defined by their willingness to go beyond loan servicing to build long-term relationships—this is what differentiates the top lending companies apart from the rest.

A Support System

Alternative lending companies like AgAmerica come up with solutions through customized loan packages that help meet the needs of the borrower and their operation for long-term production success. Stability and the ability to grow and meet the operator’s everchanging needs is an important characteristic of lenders who can offer alternative lending solutions.

Alternative Lending Isn’t

This is where much of the alternative financing stigma originates. Unconventional lending companies are not as regulated as their big bank counterparts. While this gives them the freedom of flexibility, it also leaves more room for less financially savvy farmers to be attracted into obscenely high-interest rates by companies interested in profits over people.

A Long Term Solution

Nonconventional loans are useful when an operator is in need of initial cash capital, but they should go into it with an exit strategy in place. The goal is to transition into a financial position where a more conventional loan is possible, with lower interest rates and flexible payments. AgAmerica has the unique ability to offer a spectrum of agricultural loan solutions encompassing nontraditional and traditional loan packages, depending on the specific needs and goals of the borrower.

A Short Process

Alternative lenders like AgAmerica value fostering relationships with clients and getting to know them on a deeper level. AgAmerica’s alternative finance programs provide landowners with consulting services along with working capital. These consultants will help develop a financial plan to hit their operation’s goals – often taking years, but worth the investment in the long-term.

For Any and Everyone

Be wary of alternative lending companies who will accept every application that comes their way. AgAmerica applicants go through a screening process to assess the risk factor of defaulting on a land loan. Risk assessment is necessary for determining if an applicant can be helped. If there is a risk that the hard money loan will put them in an even worse position, then they will not be accepted.

How is Alternative Lending Helping Family Farms Survive?

True ag alternative financing companies, look at the bigger picture. They pay attention to potential earnings rather than past losses. Loan specialists take the time to get to know the farmers, land, and crops to develop customized financial plans that are regularly reviewed and updated. These custom packages allow flexible payments and align with the goals of the farmer, whether it’s recovering from a natural disaster or expanding their operation. These custom loan packages have enabled U.S. farmers to refinance outstanding debt, lower debt payments, improve cash flow, and save multi-generational farms from foreclosure.

Why Family Farms in the U.S. are Important for the Economy

Simply put, family farms are the backbone of our country. But as rural areas shrink and urban areas continuously expand, many think less and less about where our food is actually coming from beyond the grocery store. Consolidating food sources into big agriculture monopolies would be detrimental to our food supply and environment. Big farms have government subsidies and payoffs keeping them in business. Smaller, multi-generational family farms are struggling to keep up. Alternative financing lenders, such as AgAmerica provide these farms with working capital so they can continue to provide the world with fresh, sustainable food.

Knowing what your options are, is critical for planning for the future. As a nationwide land lender, AgAmerica understands the challenges of farming and the obstacles farmers face. Learn how we create custom solutions for landowners and help them prepare for the long run. Speak with one of our lending experts today to learn more about our spectrum of loan options.